For Platforms & Ecosystems

- You have customers who need working capital, but no way to offer it.

- Sending leads to external lenders means losing control and revenue.

- Building in-house lending infrastructure takes years and millions in investment.

- Your merchants churn because they can't access timely credit within your ecosystem.

For MSME Lenders

- Sourcing quality MSME borrowers is expensive and time-intensive.

- You lack access to real-time transactional data for better underwriting.

- Traditional branch-based lending models can't scale to digital-first businesses.

- Co-lending partnerships are complex to structure, execute, and manage.

For Platforms

Think of us as Stripe for credit. Embed lending products into your platform without becoming a lender yourself. We handle underwriting, compliance, capital connections, and servicing.

For Lenders

Your co-lending operating system. Connect with high-quality sourcing partners, access rich transactional data, and automate the entire loan lifecycle from origination to collections.

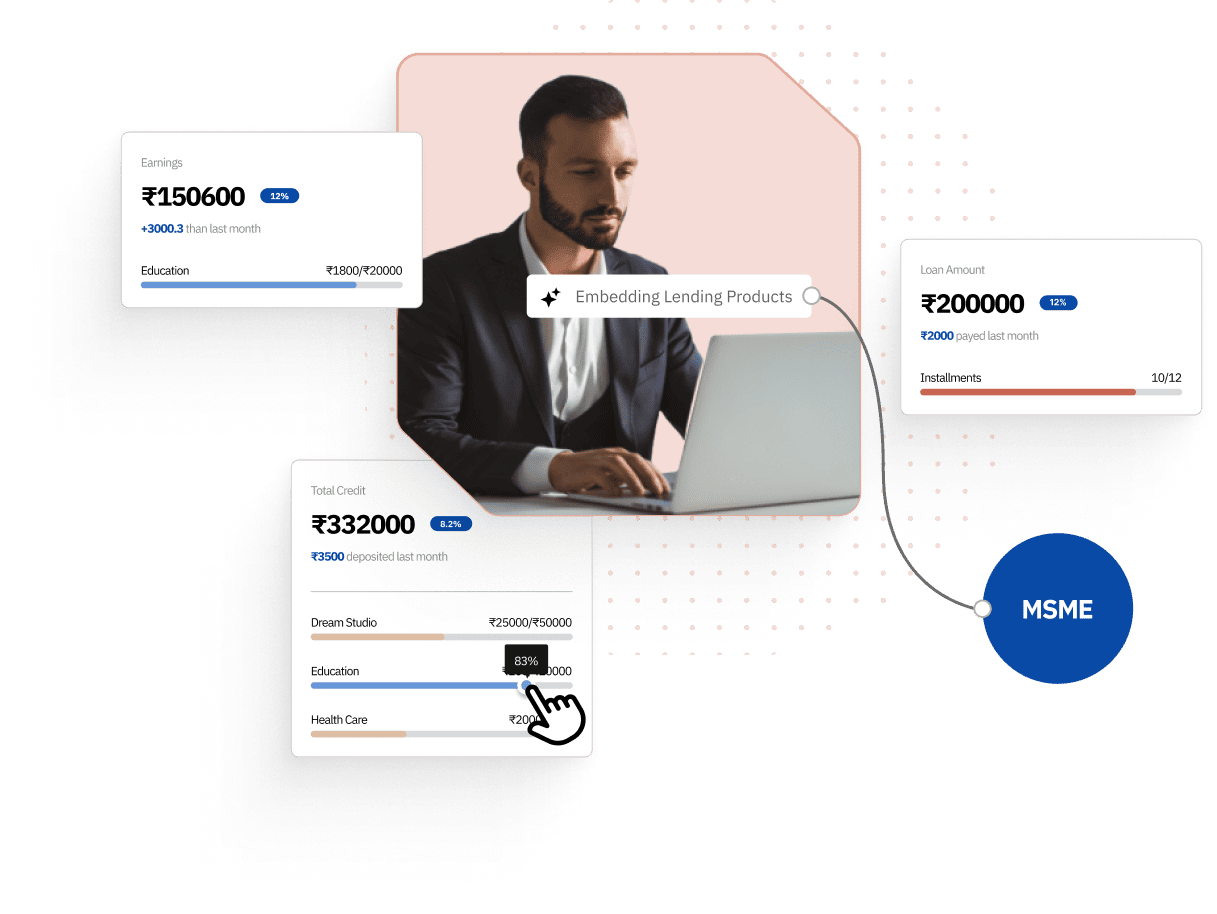

For MSMEs

They get seamless credit where they already transact. No bank visits, minimal paperwork, instant approvals based on their actual business performance.

Digital platforms, marketplaces, SaaS companies, payment gateways

What You Get:

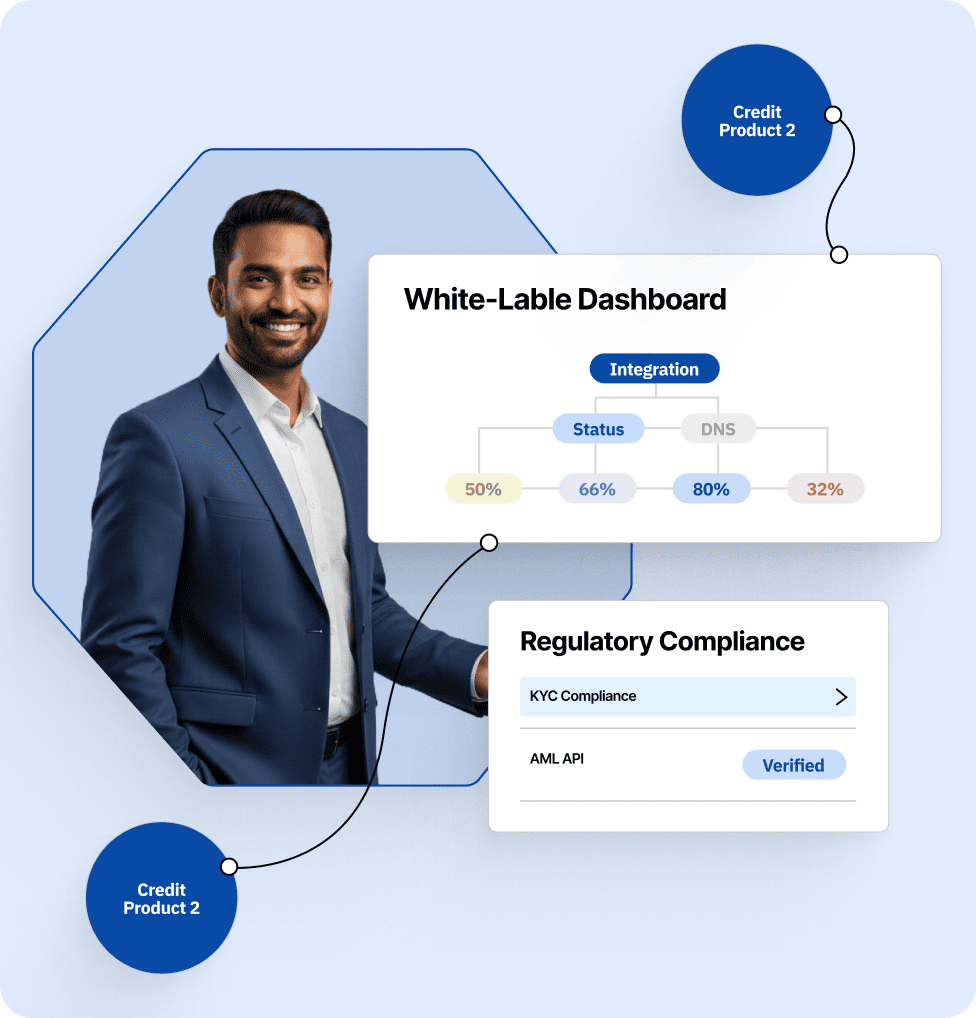

Complete infrastructure to launch credit products inside your ecosystem. White-label interfaces, automated underwriting, regulatory compliance, and access to capital—without needing an NBFC license.

Your Benefit:

New revenue stream, deeper customer relationships, reduced churn, competitive differentiation.

NBFCs, banks, financial institutions

What You Get:

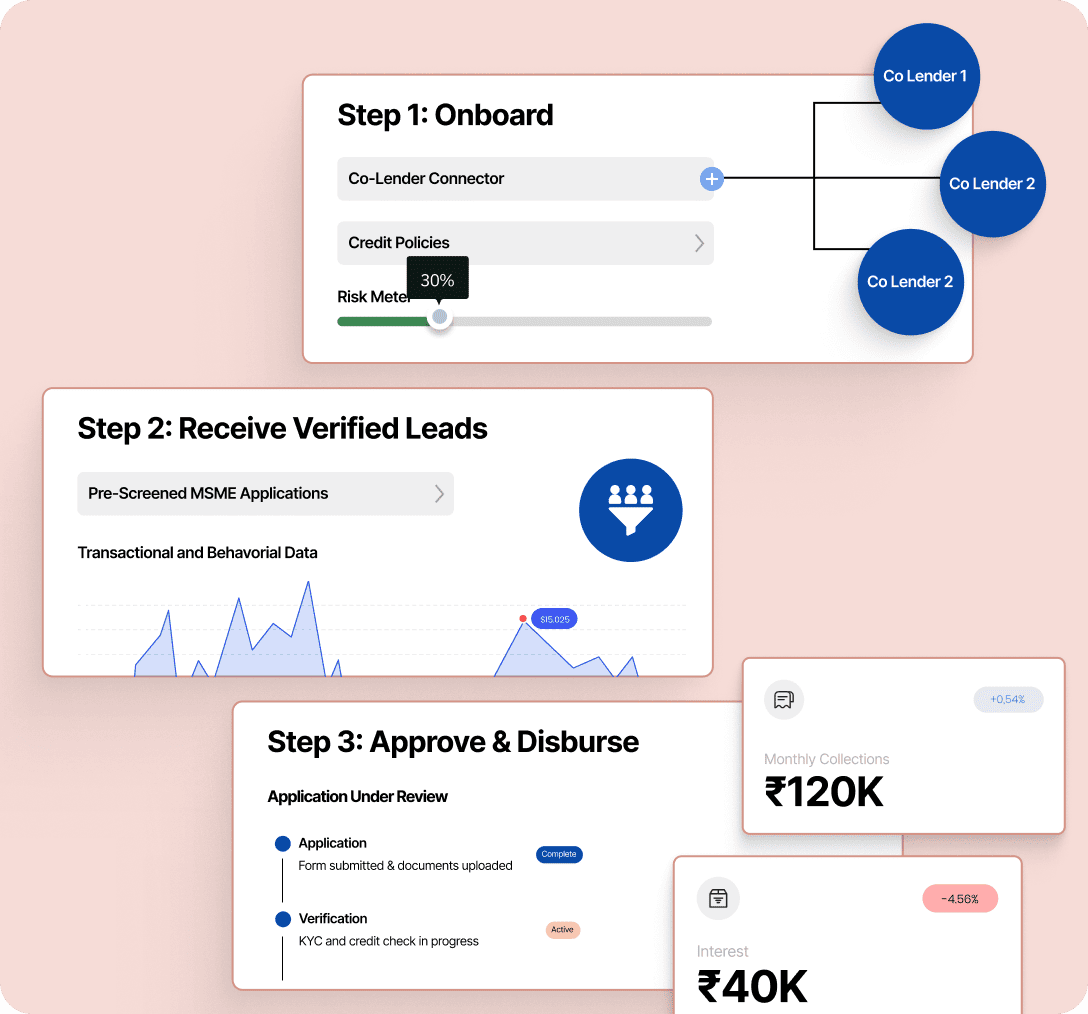

Operating infrastructure for sourcing, underwriting, and managing co-lending partnerships. Access verified MSME borrowers from digital ecosystems with rich transactional data and FLDG protection.

Your Benefit:

Lower CAC, faster growth, better risk assessment, diversified portfolio, automated operations.

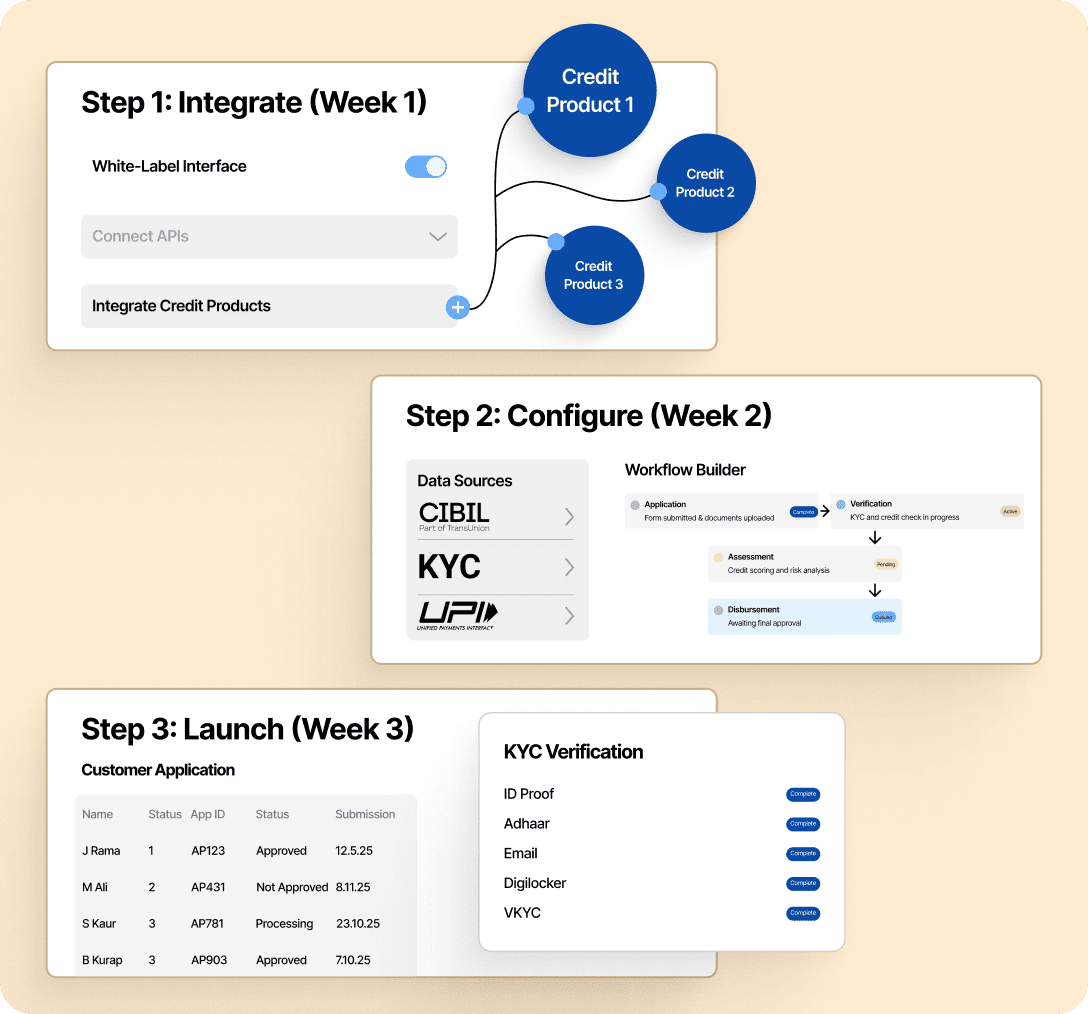

Integration & Onboarding

- RESTful APIs with comprehensive documentation.

- White-label web and mobile SDKs.

- Sandbox environment for testing.

- Webhook support for real-time updates.

- Go live in 7-14 days.

Identity & KYC

- Multi-method verification (CKYC, DigiLocker, OKYC, VKYC).

- Automated document verification.

- Consent management framework.

- Pan-India KYC coverage.

- Fully compliant with RBI guidelines.

Data & Underwriting

- 50+ third-party data integrations (bureaus, GST, bank statements).

- Real-time transactional data from platforms.

- Configurable credit scoring models.

- Automated business rule engine.

- Custom underwriting policies.

Workflow Automation

- Visual workflow builder.

- Automated decision trees.

- Exception handling and manual intervention queues.

- Multi-level approval workflows.

- Customizable for different products.

Loan Lifecycle Management

- Application to disbursement automation.

- NACH/UPI mandate setup.

- Automated repayment collection.

- Reconciliation and settlement.

- Customer self-serve portal.

Co-Lender Connector (LAMP)

- Seamless multi-lender integration.

- Automated fund routing.

- Real-time sync with lender systems.

- Portfolio monitoring.

- Early warning systems.

Risk & Compliance

- FLDG (First Loss Default Guarantee) management.

- Portfolio concentration monitoring.

- Continuous borrower performance tracking.

- Regulatory reporting.

- Complete audit trails.

Analytics & Reporting

- Real-time dashboards.

- Custom report builder.

- Portfolio analytics.

- Cohort analysis.

- Performance metrics.